Amidst a year of increasing global tea production and decreasing exports from producing countries, China continued to lead the pack in production while also taking second in exports. It also remains the dominant source of green teas along with the widest variety of types of tea, including wulong (oolong), white, yellow, and dark teas. Domestic China consumption of teas remains strong, so the forecast for the Middle Kingdom’s tea continues to look bright.

EXPORTS

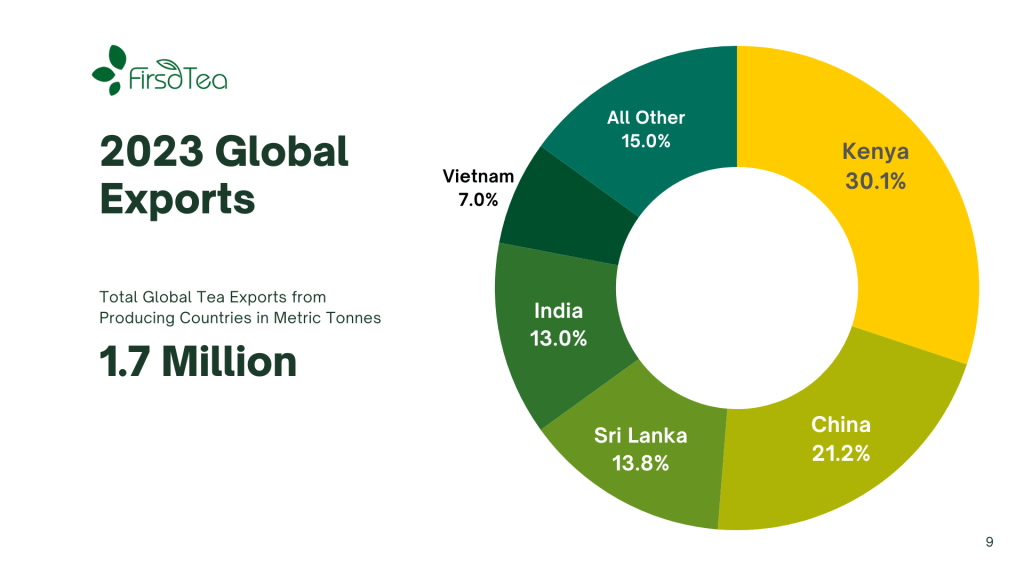

Global tea exports from producing countries declined by about 5 percent over the previous year, with China exports dipping by about 2 percent. China, however, maintained its place as the producing country with the second highest volume of exports. Kenya took the top position, having increased their exports by 14.7 percent over 2022 levels. Kenya accounted for 30.1 percent of global exports from producing countries. China’s 0.37 million metric tons (mmt) of exports accounted for 21.2 percent of global exports from producing countries, and 11 percent of China’s annual production.

84.2 percent of China’s tea export volume was green tea and the next highest volume was black tea with 7.9 percent. Green tea exports remained relatively steady compared to 2022 levels, but black tea dropped by 12.6 percent over the previous year. This rise and fall in black export volumes coincided with a few factors. Supply of Ceylon black tea dropped in 2022. When this occurred, Pakistan and other major black tea importing countries turned to China and others to meet their black tea demands. This surge stands in contrast with what occurred in other parts of the world, where tea imports increased in 2022 as buyers re-stocked after COVID created supply chain woes and then decreased their import levels in 2023 as they worked through excess inventory.

Morocco, China’s largest tea export partner, showed a similar pattern. Most years, Morocco alone takes in about 20% of China’s exports, usually around 75,000 metric tons. 2020 saw a 9.6 percent decline in Chinese tea imports. The next two years saw import volumes return to usual levels, but 2023 levels declined again by about 16 percent from 75,400 metric tons to 59,800 metric tons. Ghana, which has been the third largest export destination, increased imports by 44 percent to swap places with Uzbekistan. Taken together, these three countries import one third of China’s tea exports. Russia and the United States took in 4 and 2.3 percent of China’s exports, respectively. Import volumes were down by 25.1 percent for Russia and 33.7 percent for the U.S. Overstocking was the main culprit for these declines, particularly for the U.S. U.S. imports of Chinese teas in early 2024 are already showing signs of rebalancing.

OUTLOOK

China’s overall tea trends appear positive. Production levels are on track to increase around 4.5-5 percent based on average annual increases. Spring 2024 weather in most areas has cooperated, providing a healthy crop thus far. Development in tea producing areas, especially the Western and Central Belts, remains steady. Domestic consumer demand also appears to be on the uptick. The China tea industry has been highlighting the need for promoting demand, and recent years have seen the introduction of increased bottle teas and other tea-based RTD beverage sales. Average export prices can be expected to stay steady between $5.50 – $6.00 per kg, although labor and farm inputs (fertilizer, agrochemicals) continue to rise. Export volumes are showing signs of rebound after last year’s decline. China is poised to maintain its dominant role in global tea.