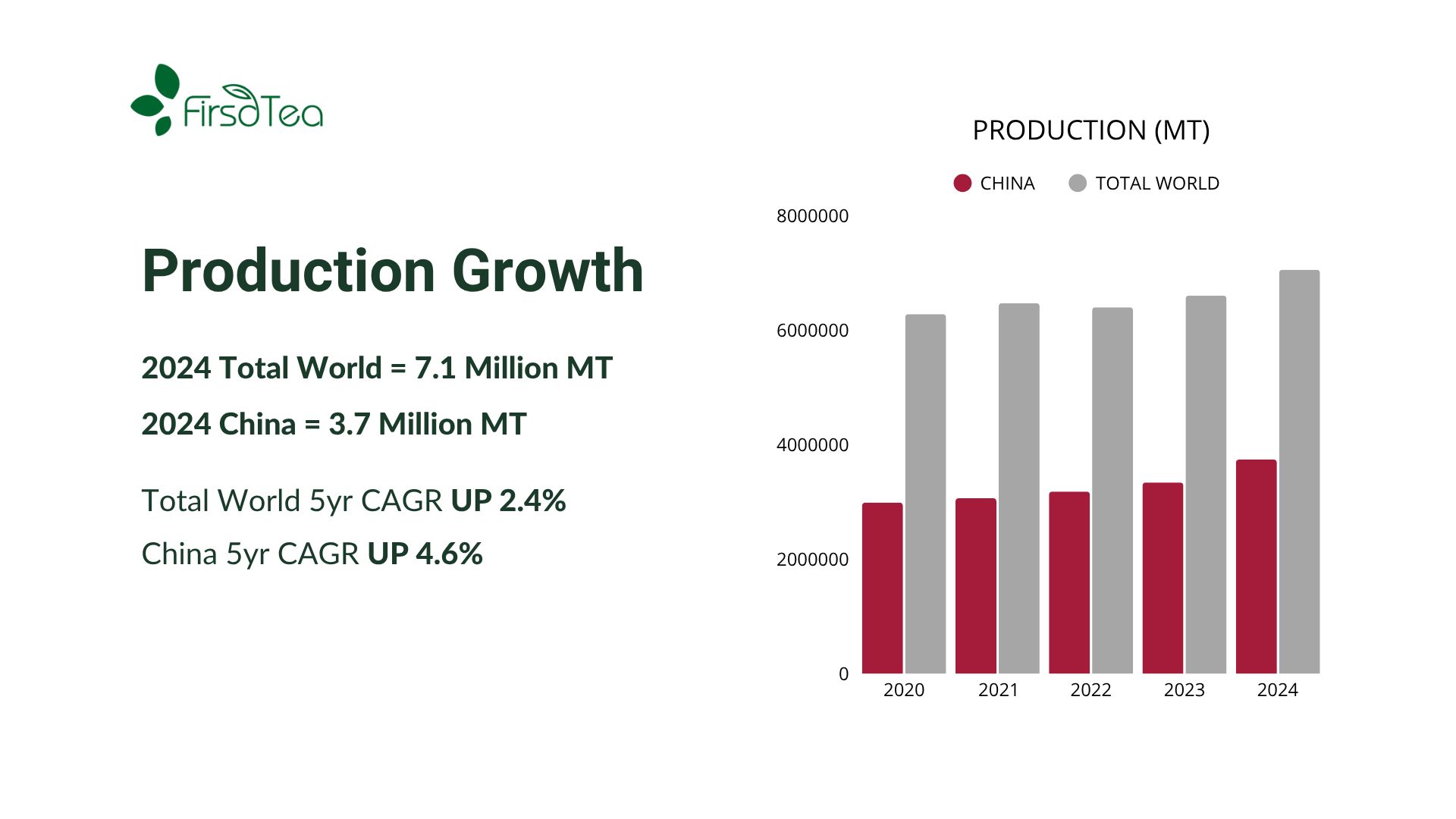

Not only did China contribute 53% of global tea production in 2024, its growth in production outpaced other major producing countries. With a compound annual growth rate of 4.6%, this far exceeded growth seen in India (0.4%), and Kenya (1.0%).

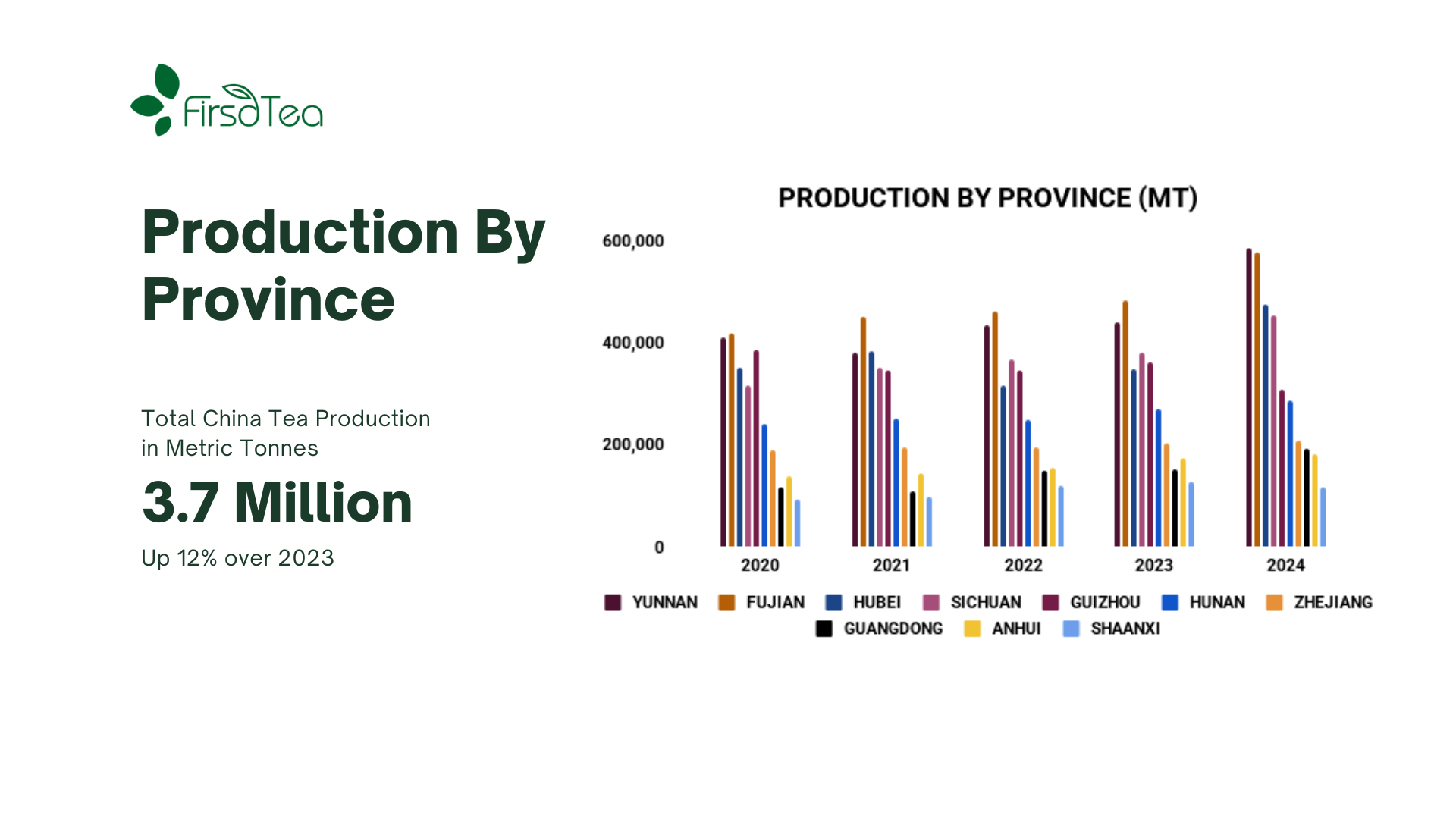

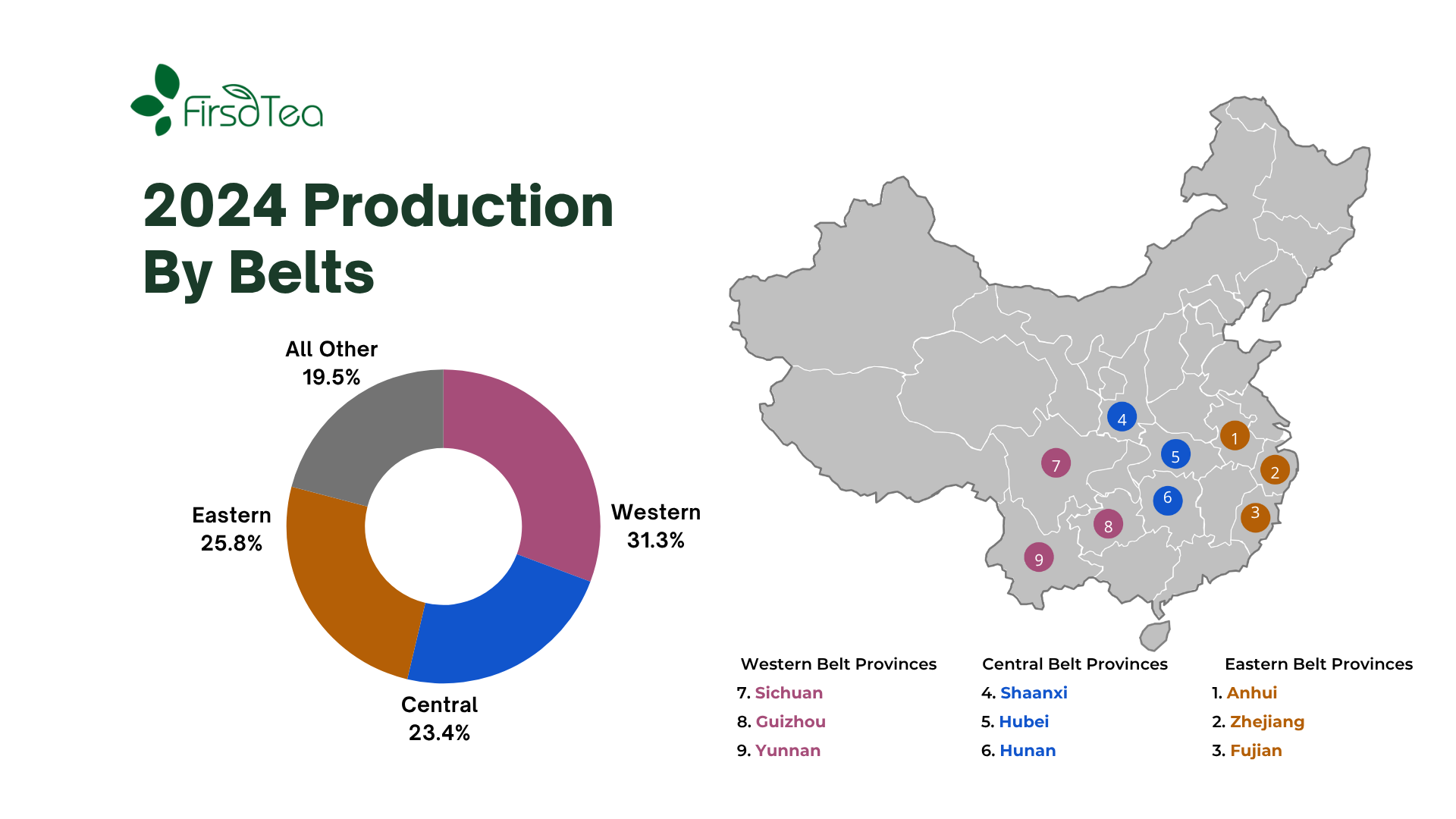

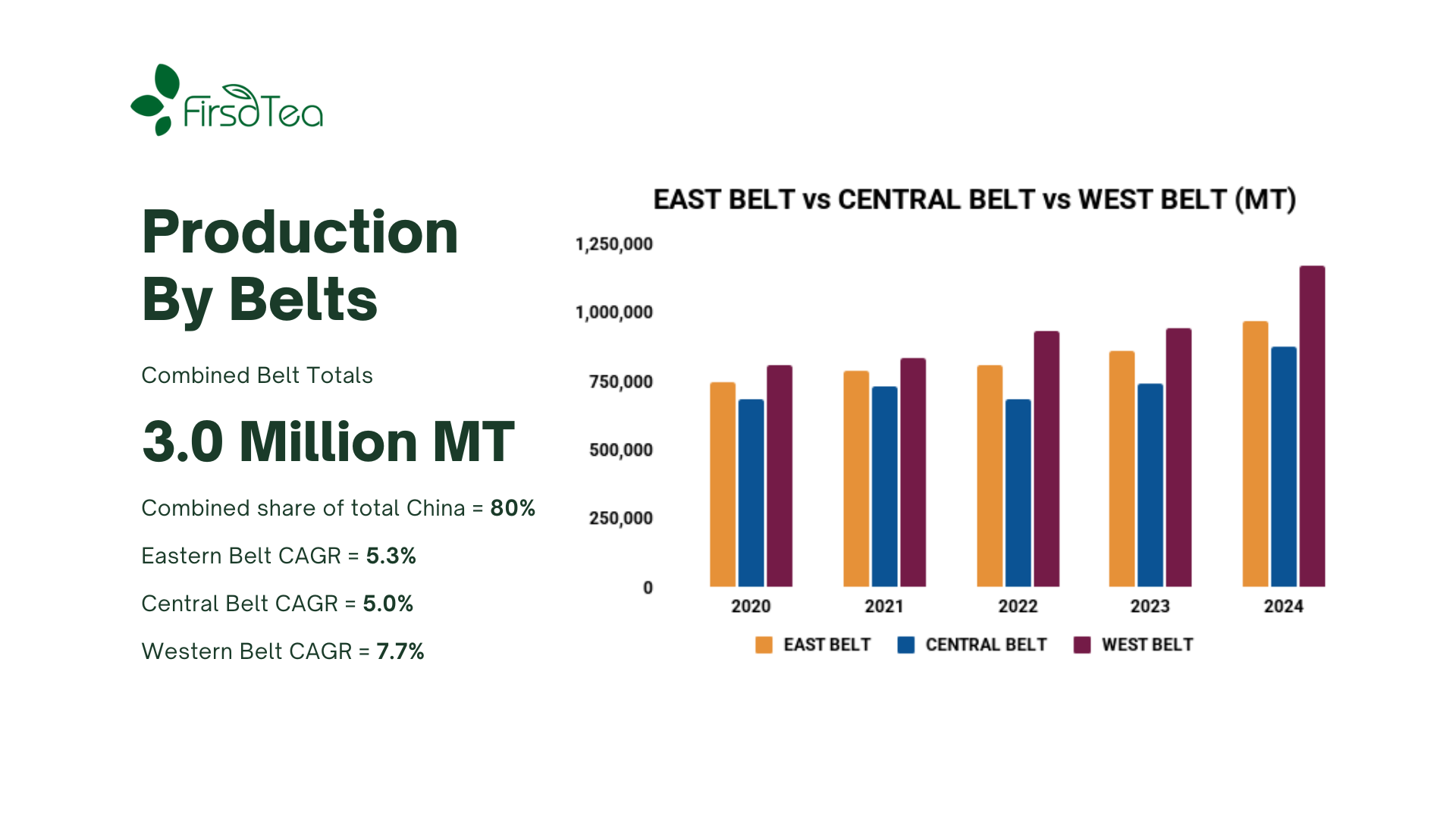

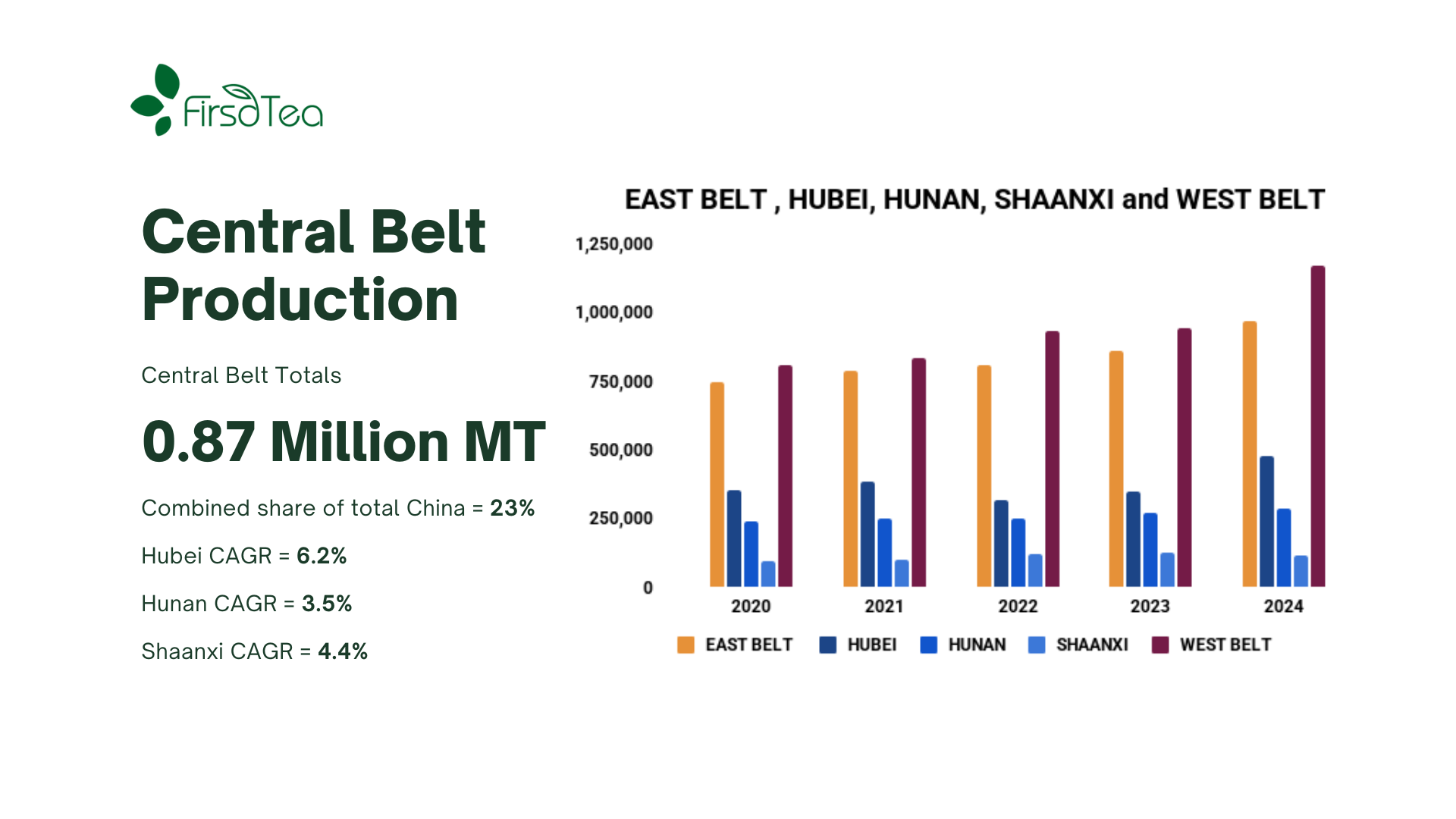

The top 10 producing provinces in China continue to show a general strengthening of production capacity, particularly among Western (purple) and Central (blue) provinces.

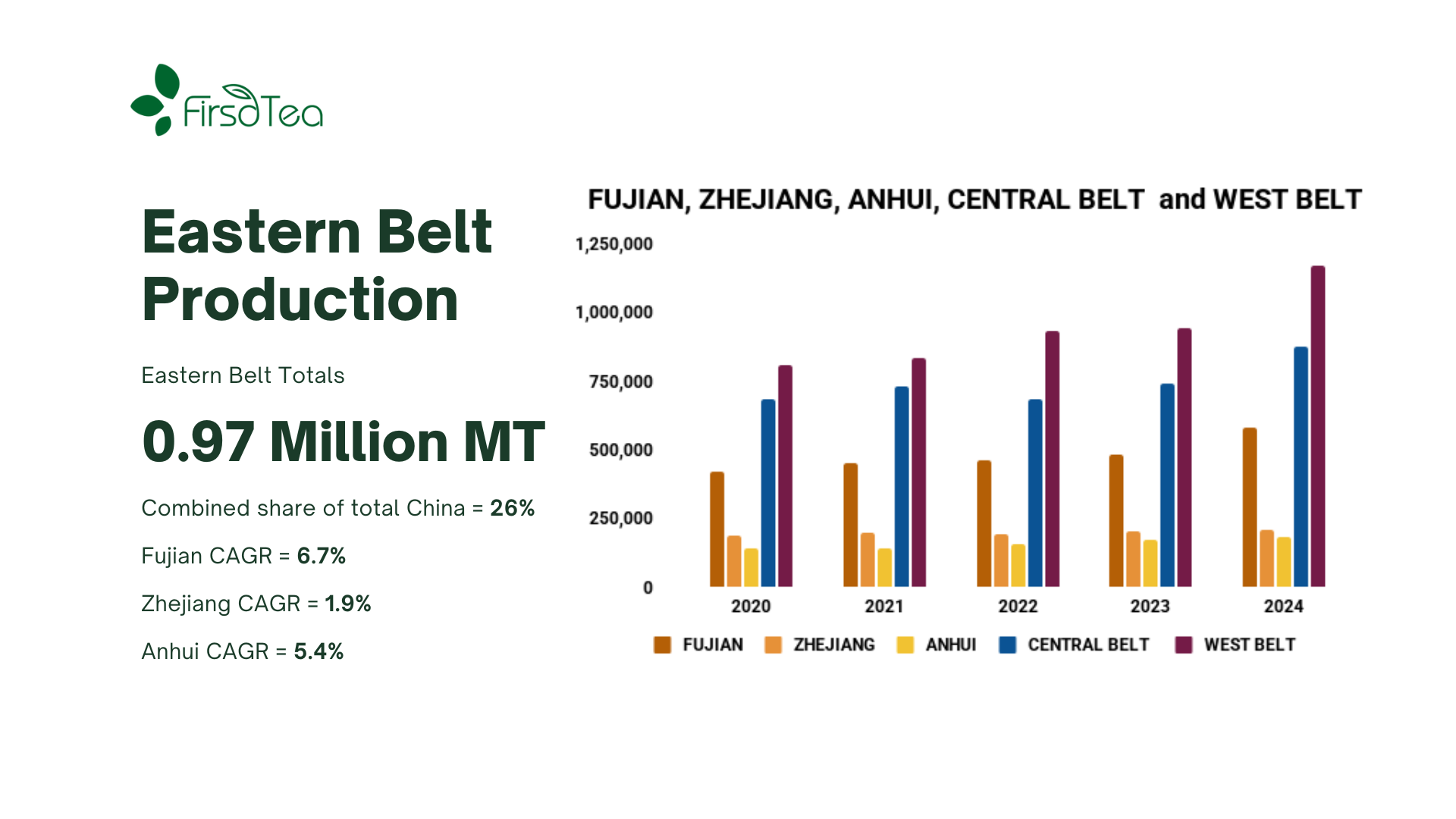

With the exception of Fujian province among the Eastern provinces, Western and Central provinces tend towards larger shares of production and same or better rates of growth than the Eastern provinces of Zhejiang and Anhui.

Looking at the breakdown of production growth by province, Shaanxi and Guizhou provinces appear weaker. However, these provinces have shown significant gains in bolstering their total acreage. 2024 data on province-level hectares is incomplete at this time, but numbers from previous years puts Guizhou province as the second-largest in terms of tea hectares, and Shaanxi province growing by as much as 1.6% per year.

OUTLOOK

Looking forward, the 2024 data points toward a positive trajectory for China tea in 2025. China’s overall production capacity continues to expand. Domestic consumption will continue to be shaped by the rise of innovative and improving tea beverage offerings- including higher quality bubble tea drinks, and bottled teas incorporating a wider range and quality of base teas. Export markets, while shifting slightly in their total volumes, appear stable overall. Tariffs will loom heavily for the US market. From China’s perspective, 0.3% of China’s annual tea production volume is exported to the U.S. Seen from the U.S. side though, China tea imports account for about 10 percent of both volume and value. The U.S. consumer stands to lose more than the Chinese seller if tariffs on tea are not stabilized at a sustainable level.