The US tea market landscape in 2025 offered ups and downs, as trends, tariffs, and regulations shaped the terrain of supply and demand.

Trade Patterns

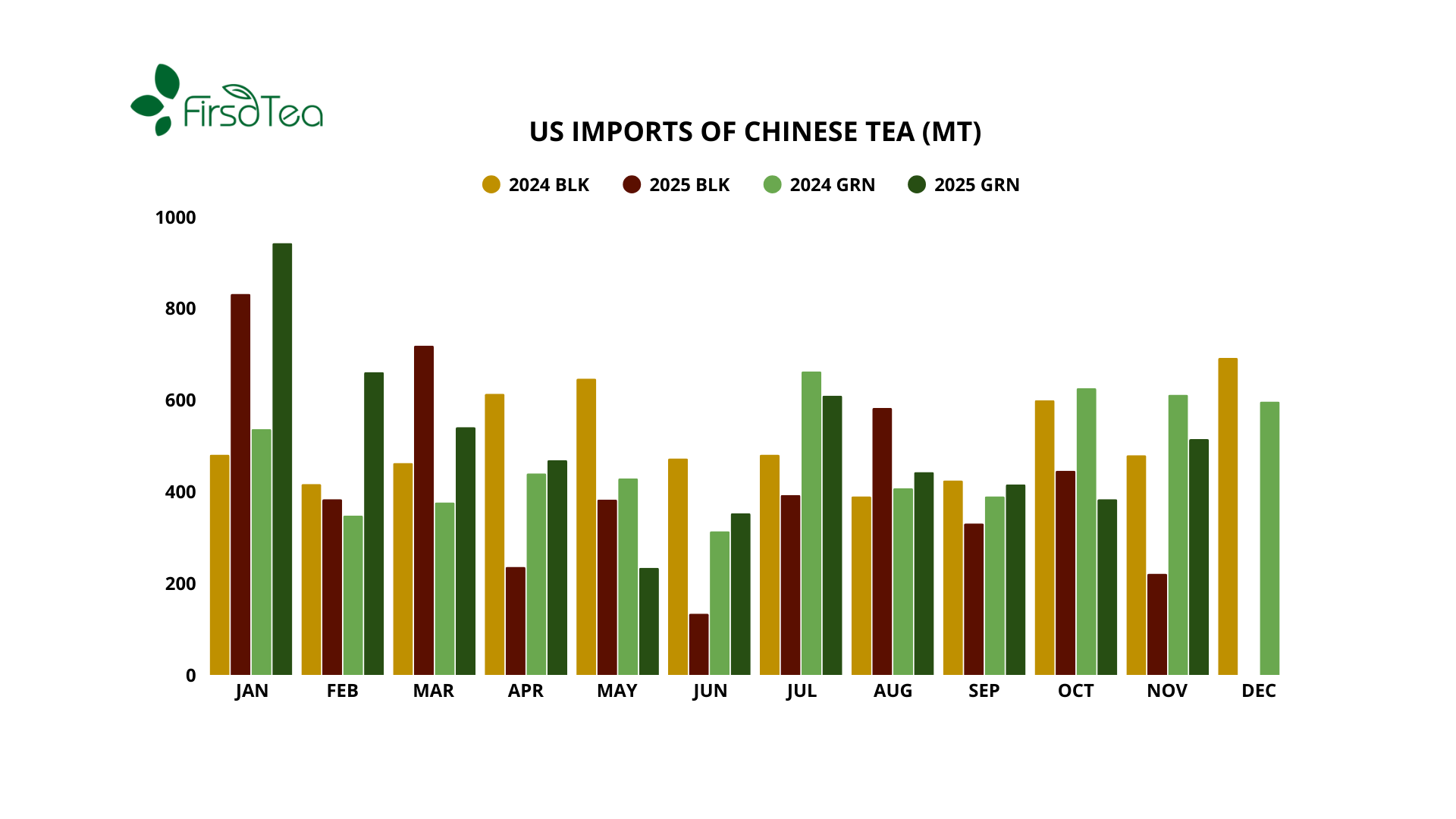

Through November 2025, the US imported 103,179 metric tons of tea, with black tea maintaining its dominant position at 86,096 MT, representing 83 percent of total imports. Argentina continued its leadership in black tea supply, accounting for 43 percent of all black tea imports at 37,296 MT. India and Vietnam rounded out the top three suppliers with 6,442 MT and 4,905 MT, respectively.

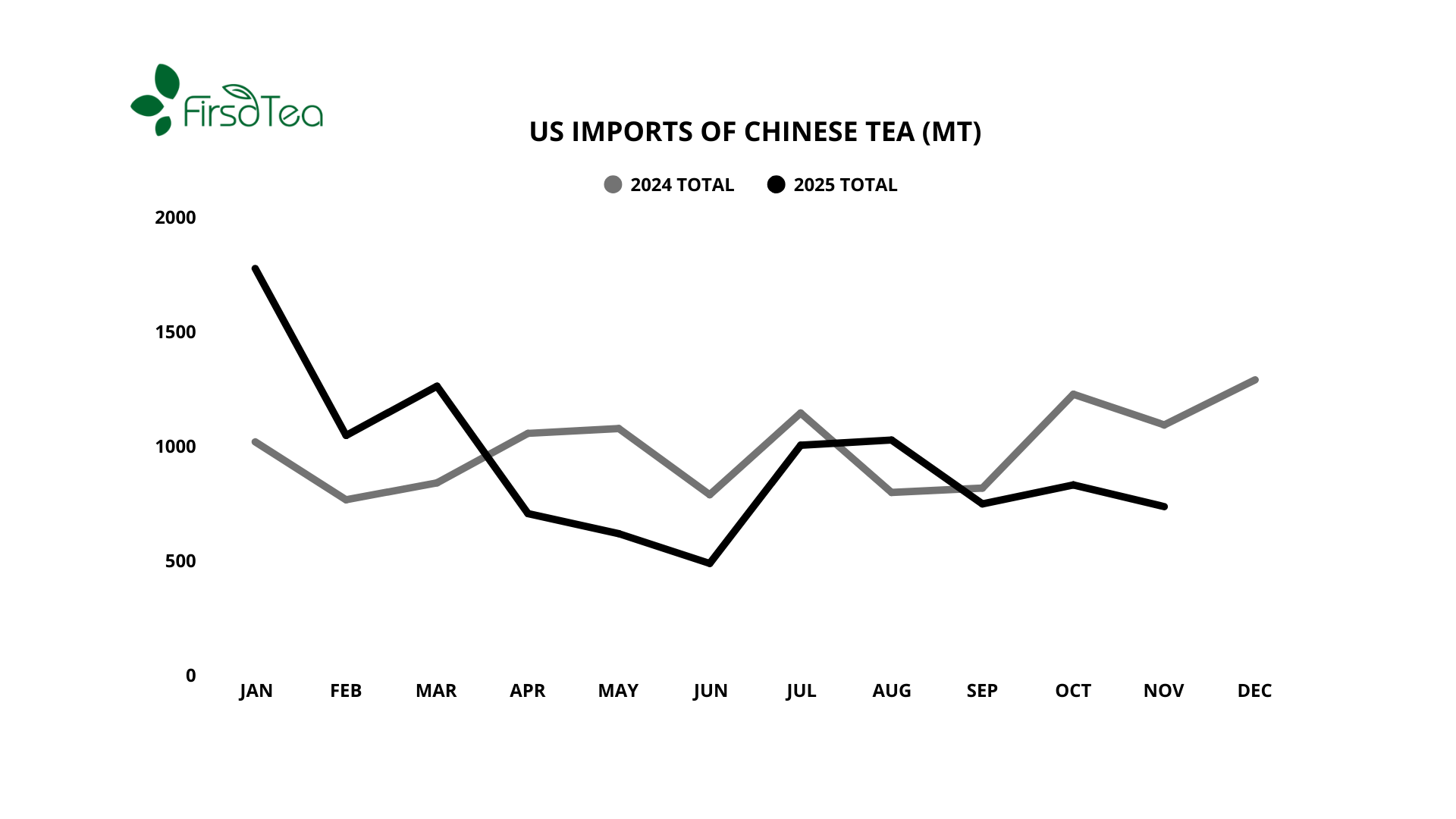

Green tea imports totaled 17,081 MT for the eleven-month period, representing 17 percent of total volume. China supplied 5,570 MT, capturing 32.6 percent of the green tea segment with an 8.1 percent increase over 2024 levels. Japan demonstrated particularly strong growth, exporting 4,189 MT to the US market—a 38 percent year-over-year increase that accounted for just shy of a quarter of total green tea imports.

Matcha Madness

If 2025 were expressed as a popular tea drink, it would be the matcha latte. Matcha deserves at least partial credit for the significant increase in Japanese green tea imports over the previous year. Conservative estimates place 2024 Japanese matcha imports at approximately 2.5 tons, with 2025 figures expected to show substantial growth when final data becomes available.

The surge in demand has created supply pressures. Insiders believe that the vast majority of Japan’s 2026 matcha have already been contracted, leaving buyers to look elsewhere to secure any further quantities.

Tariff Turbulence

Tariff rate volatility created trade instability in 2025. Following President Trump’s inauguration on January 20, a series of tariff increases affected tea imports from multiple origins, with China-sourced tea experiencing the most dramatic shifts. Rates on Chinese tea peaked at 152.5 percent before declining to 17.5 percent by year’s end.

Importers responded to these tariffs with increased buying early in the year to bring in move volume before the higher rates came into effect. The middle of the year saw import volumes slump, as the industry drew down on those reserves, or otherwise avoided bringing in new supply.

Tea as Real, and Healthy

Policy shifts also created opportunities for stronger messaging to tea consumers. Certain tea products, particularly unsweetened varieties, gained greater recognition for their role in a balanced diet. New dietary guidelines were rolled out, emphasizing “whole” and “real” foods, and unsweetened teas began to be referenced as an “optimal beverage.” This shift coincides with growing research on flavan-3-ols, bioactive compounds abundant in tea that have been linked to reduced cardiometabolic disease risk.

The research connecting flavan-3-ols to improved health outcomes related to obesity, diabetes, hypertension, and cholesterol management provides favorable positioning to tea as consumers grow greater appreciation for functional beverages.

Looking Ahead

Some of the forces at work in 2025 will likely extend into 2026. Without action from the Supreme Court or Congress, tariff rates will rise and fall at the discretion of the President. The popular momentum of matcha does not appear to be losing steam, and the overall tea trade keeps humming along. Overall, tea remains an affordable, accessible, and (potentially) healthy beverage for millions of Americans.