HARVEST AND PROCESSING: CHINA VS. JAPAN

JAPAN

Based on Japan’s government data and industry analysis, Japan’s matcha production capacity appears insufficient relative to its export volume. Japan’s harvestable tea fields totaled 25,400 hectares in 2025, a 30% reduction over the past decade. Overall agricultural labor supply in Japan has also dropped by about 25% between 2020 and 2025. Japan’s matcha production reached approximately 4,000 tons, which puts the current export volume of 8,700 tons in a complicated light. The gap suggests Japan is supplementing its domestic leaf supply with base green tea leaf sourced from China and elsewhere to meet demand.

Traditional tencha-ro (碾茶炉) brick stoves, used in the drying of tencha leaf, are capable of processing around 0.8 metric tons per day. Quality advocates argue that this method yields richer, more complex umami characteristics. Modern equipment can produce roughly double that volume per day, though increased throughput does not always preserve the same flavor depth.

CHINA

In 2025, China boasted matcha production of 12,000 tons, or roughly 70% of total global production for the year. Since then, China has continued to boost both its production area and infrastructure. Active matcha production lines have grown from 120 to nearly 600. Tencha leaf volumes have increased threefold at more standard quality levels, and roughly 1.5 times at higher-grade levels. Guizhou and Hubei provinces have been the primary drivers of this growth, while Zhejiang province remains a leader in total volume and is recognized for its higher quality standards.

Not all production lines are equivalent, and the quality ceiling varies significantly depending on the equipment and techniques employed across these locations. Newer lines can be more consistent in output but may lack the character associated with traditional processing methods.

Products marketed as matcha can result from varying production standards. Some producers skip the traditional shading step for tencha leaf prior to harvest. In other cases, pan-fired leaf is blended with steamed leaf to extend available volumes. A further alternative is moga-cha, a milled tea produced from sencha rather than shade-grown tencha. Its flavor profile has less of the marine and umami character typical of matcha, though it provides a comparable green color. These practices are generally responses to supply pressure rather than an intent to deceive. In beverage applications that include sweeteners and dairy, the distinction is less noticeable to the end consumer.

EXPORTS: CHINA VS. JAPAN

JAPAN

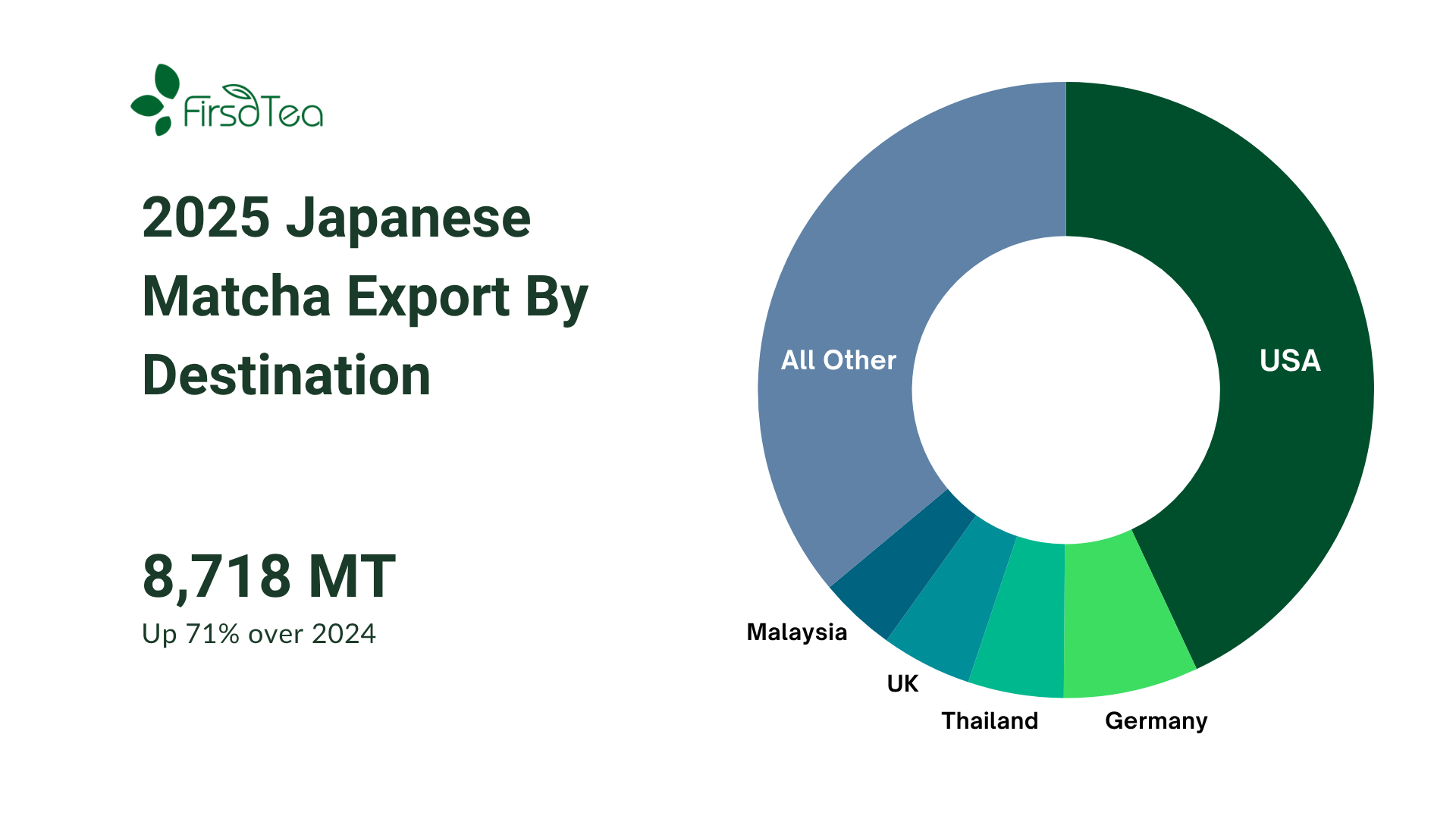

Japan exported 8,700 tons of powdered green tea in 2025, a 71% increase over the prior year. The United States was the dominant destination, accounting for over 50% of total export volume. The EU followed, and Southeast Asia (particularly Thailand and Malaysia) also received meaningful volumes as innovative matcha-based beverages have found a strong following in those markets.

In 2024, Japan exported approximately 5,092 tons of matcha valued at around $185 million USD. The US alone received 2,217 tons at an average of $39.37/kg. The acceleration since then reflects sustained global appetite.

CHINA

China’s role in matcha exports has expanded dramatically. In the first quarter of 2026, exports of matcha from Zhejiang province were estimated to be 1,200 tons, although dedicated national export statistics for matcha are not maintained separately. Chinese matcha is primarily destined for food service and beverage manufacturing, where it is valued for its affordability and availability at scale. The rapid expansion of boba tea chains across Eastern Asia has driven particularly strong regional demand, and China’s geographic and logistical proximity gives it a clear advantage in supplying those markets.

OUTLOOK: CHINA VS. JAPAN SUPPLY GOING FORWARD

JAPAN

Japan’s supply position is constrained. Harvestable acreage has been declining for a decade, and domestic processing capacity sits well below current export volumes. The bulk of Japan’s matcha crop is now contracted well in advance, often before the harvest season begins.

Buyers seeking Japanese matcha, particularly those with quality specifications tied to provenance or specific cultivars, are advised to plan and contract early. Spot availability is limited, and pricing continues to reflect tight supply relative to demand.

CHINA

China is positioned as the primary lever for meeting global matcha demand going forward. Guizhou Province alone has committed to establishing over 13,000 hectares of dedicated tencha fields, with a processing capacity target of 8,000 tons annually. For comparison, all of Japan’s harvestable tea fields cover 25,400 hectares across all tea types.

China’s expansion suggests that supply relief is coming, though quality differentiation will remain a significant consideration. As production scales further, buyers will benefit from understanding the range that exists within Chinese matcha: from high-grade shaded tencha processed on traditional lines, to commodity-grade products intended for beverage manufacturing.

FURTHER NOTE: SENCHA SUPPLY CONTRAINTS

One adjacent effect worth watching is sencha availability. The most common cultivar used for both matcha and sencha production in Japan and China is yabukita (薮北). As producers converted sencha fields to tencha production to capture matcha demand, sencha supply has tightened. Earlier harvests shaded for tencha left less leaf available for sencha processing. The matcha boom has created a sencha undersupply as a secondary consequence. In actual fact, any and all organic Chinese green teas may face additional strain as pressures for raw leaf and processing activity draw these resources towards matcha and away from other green tea activities.

The overall picture is one of a market adapting quickly to extraordinary demand, with China absorbing the bulk of the volume requirement, Japan holding its position at the quality tier, and the entire supply chain under pressure to deliver more, faster, and at acceptable quality for an increasingly matcha-hungry global market.